Exhibit 99.2 Confidential SynCardia, a subsidiary of Picard Medical Total Artificial Heart, Viable Alternative to Heart Transplants 24 April 2023 Preliminary |

Disclaimer (1/2) THIS PRESENTATION (TOGETHER WITH ORAL STATEMENTS MADE IN CONNECTION HEREWITH, THIS “PRESENTATION”) IS BEING PROVIDED TO YOU SOLELY FOR YOUR INFORMATION. THIS PRESENTATION HAS NOT BEEN APPROVED BY ANY REGULATORY AUTHORITY. THIS PRESENTATION DOES NOT CONSTITUTE AN OFFER TO SELL OR ISSUE, OR ANY SOLICITATION OF ANY OFFER TO PURCHASE, SUBSCRIBE FOR OR OTHERWISE AQCQUIRE, ANY SECURITIES IN ANY STATES OR JURISDICTIONS IN WHICH SUCH OFFER, SOLICITATION OR SALE WOULD BE UNLAWFUL, AND NOTHING CONTAINED HEREIN SHALL FORM THE BASIS OF ANY CONTRACT OR COMMITMENT WHATSOEVER. THIS PRESENTATION MAY NOT BE PUBLISHED OR FURTHER DISTRIBUTED, DIRECTLY OR INDIRECTLY, IN WHOLE OR IN PART, TO ANY OTHER PERSON IN ANY JURISDICTION WHERE, OR TO ANY OTHER PERSON TO WHOM, TO DO SO WOULD BE UNLAWFUL. This Presentation is only being provided to assist interested parties in making their own evaluation with respect to the proposed business combination (the “Business Combination” between Altitude Acquisition Corp. (“Altitude”) and Picard Medical, Inc. (the “Company”). References to the Company include the Company and its subsidiaries, including SynCardia Systems, LLC (“SynCardia”). The information contained herein does not purport to be all-inclusive and none of Altitude, the Company, or any of their respective affiliates nor any of its or their control persons, officers, directors, employees or representatives makes any representation or warranty, express or implied, as to the accuracy, completeness or reliability of the information contained in this Presentation. You should consult your own counsel and tax and financial advisors as to legal and related matters concerning the matters described herein, and, by accepting this Presentation, you confirm that you are not relying upon the information contained herein to make any decision. The reader shall not rely upon any statement representation or warranty made by any other person, firm or corporation (including, without limitation, Altitude, the Company, or any of their respective affiliates or control persons, officers, directors and employees) in making its investment or decision to invest. None of Altitude, the Company, any of their respective affiliates nor any of its or their control persons, officers, directors, employees or representatives, shall be liable to the reader for any information set forth herein or any action taken or not taken by any reader, including any investment in shares of Altitude or the Company. Forward-Looking Statements This Presentation contains statements that are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements include all statements that do not relate solely to historical or current facts and can generally be identified by the use of future dates or words such as “may,” “should,” “could,” “will,” “expects,” “seeks to,” “anticipates,” “plans,” “believes,” “estimates,” “intends,” “predicts,” “projects,” “forecast,” “potential” or “continue” or the negative of such terms and other comparable terminology. These statements are not guarantees of future performance and involve risks, uncertainties and assumptions that are difficult to predict. Therefore, actual outcomes and results may differ materially from what is expressed or forecasted in such forward-looking statements due to numerous factors, risks, and uncertainties that could cause actual results to differ materially from such estimates or forecasts. You are cautioned not to unduly rely on such forward-looking statements when evaluating the information in this Presentation. Such forward-looking statements speak only as of the date on which they are made and Altitude and the Company do not undertake any obligation to update any forward-looking statement to reflect events or circumstances after the date of this Presentation. Forward-looking statements in this presentation may include, for example, statements about: the Company’s growth strategy, future operations, financial position, estimated revenues and losses, projected capex, prospects and plans; the Company’s strategic advantages and the impact those advantages will have on future financial and operational results; the implementation, market acceptance and success of the Company’s products; the Company’s approach and goals with respect to research and development; the Company’s expectations regarding its ability to obtain and maintain intellectual property protection and not infringe on the rights of others; changes in applicable laws or regulations; and the outcome of any known and unknown litigation and regulatory proceedings. Neither Altitude, the Company nor any of its subsidiaries, affiliates, representatives or advisors assumes any responsibility for or makes any representation or warranty (express or implied) as to, the reasonableness, completeness, accuracy or reliability of the estimates and information contained herein, which speak only as of the date identified on the cover page of this Presentation. Altitude, the Company and their respective affiliates, representatives and advisors expressly disclaim any and all liability based, in whole or in part, on such information, errors therein or omissions therefrom. Neither Altitude, the Company nor any of their respective affiliates, representatives or advisors intends to update or otherwise revise the estimates and other information contained herein to reflect circumstances existing after the date identified on the cover page of this Presentation to reflect the occurrence of future events even if any or all of the assumptions, judgments and estimates on which the information contained herein is based are shown to be in error, except as required by law. Confidential 2 2

Disclaimer (2/2) Industry and Market Data In this Presentation, we rely on and refer to information and statistics regarding market participants in the sectors in which the Company competes and other industry data. We obtained this information and statistics from third-party sources, including reports by market research firms and publicly-available filings. While we believe such third- party information is reliable, there can be no assurance as to the accuracy or completement of the indicated information. We have not independently verified the accuracy or completeness of the information provided by the third-party sources. Trademarks This Presentation contains trademarks, service marks, trade names and copyrights of the Company and other companies, which are the property of their respective owners. Solely for convenience, some of the trademarks, service marks, trade names and copyrights referred to in this Presentation may be listed without the TM, SM, © or ® symbols, but the Company will assert, to the fullest extent under applicable law, the rights of the applicable owners, if any, to these trademarks, service marks, trade names and copyrights. Further, third-party logos included in this Presentation may represent past or present vendors or suppliers of materials and/or products to the Company for use in connection with its business or may be provided simply for illustrative purposes only. Inclusion of such logos does not necessarily imply affiliation with or endorsement by such firms or businesses. There is no guarantee that the Company will work, or continue to work, with any of the third parties whose logos are included herein in the future. Additional Information and Where to Find It This document relates to a proposed Business Combination between Altitude and the Company. In connection with the proposed Business Combination, Altitude intends to file with the SEC, a registration statement on Form S-4, containing a preliminary proxy statement/prospectus of Altitude and after the registration statement is declared effective, Altitude will mail a definitive proxy statement/prospectus relating to the proposed Business Combination to its stockholders. This Presentation does not contain any information that should be considered by Altitude’s stockholders concerning the proposed Business Combination and is not intended to constitute the basis of any voting or investment decision in respect of the Business Combination or the securities of Altitude. Altitude’s stockholders and other interested persons are advised to read, when available, the preliminary proxy statement/prospectus and the amendments thereto and the definitive proxy statement/prospectus and other documents filed in connection with the proposed Business Combination, as these materials will contain important information about Altitude, the Company and the Business Combination. When available, the definitive proxy statement/prospectus and other relevant materials for the proposed Business Combination will be mailed to stockholders of Altitude as of a record date to be established for voting on the proposed Business Combination. Stockholders will also be able to obtain copies of the preliminary proxy statement/prospectus, the definitive proxy statement/ prospectus and other documents filed with the SEC, without charge, once available, at the SEC’s website at www.sec.gov, or by directing a request to: Altitude Acquisition Corp., 400 Perimeter Center Terrace, Suite 151, Atlanta, GA 30346. Participants in the Solicitation Altitude, the Company and their respective directors, executive officers, other members of management and employees may be deemed participants in the solicitation of proxies from Altitude’s stockholders with respect to the proposed Business Combination. Investors and security holders may obtain more detailed information regarding the names and interests in the proposed transaction of Altitude’s directors and officers in its filings with the SEC, including, when filed with the SEC, the preliminary proxy statement/prospectus and the amendments thereto, the definitive proxy statement/prospectus, and other documents filed with the SEC. Such information with respect to the Company’s directors and executive officers will also be included in the proxy statement/prospectus. Confidential 3 3

Risk Factors The risks presented below are certain of the general risks related to the Company, SynCardia, Altitude, and the proposed business combination among the Company, Altitude and their respective subsidiaries, as applicable (the “Business Combination”), and such list is not exhaustive. You should carefully consider these risks and uncertainties, carry out your own diligence, and consult with your own financial and legal advisors concerning the risks and suitability of an investment in this offering before making an investment decision. Risks relating to the business of the Company will be disclosed in future documents filed or furnished by SynCardia and Altitude with the U.S. Securities and Exchange Commission (“SEC”), including the documents filed or furnished in connection with the Business Combination. The risks presented in such filings will be consistent with those that would be required for a public company in its SEC filings, including with respect to the business and securities of the Company and Altitude and the Business Combination, and may differ significantly from, and be more extensive than, those presented below. Risks Related to Our Business • We have a history of significant losses. If we do not achieve and sustain profitability, our financial condition could suffer. • All of our revenue is generated from a limited number of products, and any decline in the sales of these products or failure to gain market acceptance of these products will negatively impact our business. • The manufacturing process of the SynCardia Total Artificial Heart (TAH) is complex and requires sophisticated equipment, experienced manufacturing personnel and highly specialized knowledge. If we are unable to manufacture the TAH on a timely basis consistent with its quality standards, our results of operations will be adversely impacted. • We rely on specialized suppliers for key components of the SynCardia TAH and related drivers and do not have second-source suppliers for the majority of the SynCardia TAH’s components. • The future worldwide demand for our current products and future products is unproven. Our current products and future products may not be accepted by hospitals, surgeons or patients, and may not become commercially successful. • If we are unable to educate physicians on the safe and effective use of the SynCardia TAH, we may be unable to achieve our expected growth. • If we fail to develop and retain a direct sales force and effective network of international distributors, we may be unable to achieve expected growth targets and our business could suffer. • Reliance on distributors and third-parties to market and sell our products could negatively impact our business, because we may not be able to find suitable distributors for our products on satisfactory terms, agreements with distributors may prematurely terminate, our existing distributor relationships or contract may preclude us or limit us from entering into arrangements with other distributors, and we may not be able to negotiate new or renew existing distributing agreements on acceptable terms, or at all. • We operate in a highly competitive market segment, which is subject to rapid technological change. If our competitors are able to develop and market technologies or products that are safer, more effective, less costly, easier to use or otherwise more attractive than our products, our business will be adversely impacted. • We have significant customer concentrations, and economic difficulties or changes in the purchasing policies or patterns of our key customers could have a significant impact on our business and operating results. We have no long-term exclusive agreements with our customers and, as a result, generally operate on an invoice and purchase order basis to meet our customers’ needs. • Our future success depends on our ability to develop, receive regulatory approval for, and introduce new products or product enhancements that will be accepted by the market. • If we are unable to successfully complete the pre-clinical studies or clinical trials necessary to support premarket approval applications or PMA supplements, its ability to obtain approvals for new products will be limited. • If third-party payors do not provide adequate coverage and reimbursement for the use of our products, it is unlikely that our products will be widely used and our revenues will be negatively impacted. • Our manufacturing operations, research and development activities, and corporate headquarters, are currently based at a single location, which may subject us to a variety of risks. • Product liability claims could damage our reputation or adversely affect our business. • Product deficiencies could result in field actions, recalls, substantial costs and write-downs; these could also lead to the delay or termination of ongoing trials and harm our reputation and our business and financial results. • Any claims relating to improper handling, storage or disposal of hazardous chemicals and biomaterials could be time-consuming and costly to address. • Our international operations subject us to certain operating risks, which could adversely impact our results of operations and financial condition. Confidential 4 4

Risk Factors Risks Related to Our Business (Continued) • We are subject to credit risk from our accounts receivable related to its product sales, which include sales within foreign countries that have recently experienced economic turmoil. • We are subject to risks associated with currency fluctuations, and changes in foreign currency exchange rates could impact its results of operations. • Our ability to use net operating losses to offset future taxable income may be subject to certain limitations; in addition, we may be unable to use a substantial part of our net operating losses if we do not attain profitability in an amount necessary to offset such losses. • The industry- and market-related estimates included in this Presentation are based on various assumptions and may prove to be inaccurate. • Our ability to maintain our competitive position depends on our ability to attract and retain highly qualified personnel. • If we acquire other companies or businesses, form joint ventures or partner with companies in other jurisdictions, we will be subject to risks that could hurt our business. • Failure to protect our information technology infrastructure against cyber-based attacks, network security breaches, service interruptions, or data corruption could significantly disrupt our operations and adversely affect our business and operating results. • There can be no assurance that Altitude or the Company will be able to raise sufficient capital to consummate the Business Combination. Even if we consummate the Business Combination, we will need substantial additional funding to pursue our business objectives and continue our operations. If we are unable to raise capital when needed or on attractive terms, we may be required to delay, limit, reduce, or terminate our research or product development programs or future commercialization efforts. Risks Related to Regulation of Our Industry • Our business is subject to extensive governmental regulation that could make it more expensive and time consuming to introduce new or improved products. • The off-label use or misuse of our products may harm our image in the marketplace, result in injuries that lead to product liability suits, which could be costly to our business, or result in costly investigations and regulatory agency sanctions if we are deemed to have engaged in such promotion. • We are required to comply with medical device reporting, or MDR, requirements and must report certain malfunctions, deaths, and serious injuries associated with our products, which can result in voluntary corrective actions or agency enforcement actions. • Our employees, independent contractors, principal investigators, consultants, commercial partners and suppliers may engage in misconduct or other improper activities, including non-compliance with regulatory standards and requirements. • We are subject to various federal, state and foreign healthcare laws and regulations, and a finding of failure to comply with such laws and regulations could have a material adverse effect on our business. • The TAH is currently approved in the U.S. for temporary bridge to transplant indication. We plan to seek approval for long-term indication. If we do not receive that approval, we may need to undertake additional clinical trials, which could cost significant funds and adversely affect our business. • In Europe, following a suspension, we voluntarily withdrew our CE certificate under the European Union Medical Device Directive (the “CE MDD”) in 2022 and terminated our relationship with our CE notifying body, and failure to reinstate our CE certificate under CE MDR or to establish a relationship with a new notifying body could have a material adverse effect on our business. • Prior weaknesses in our CE MDD regulatory regime and compliance with developing European Union medical device regulations, including the CE MDD, may limit our ability to market or sell products in European markets or to introduce new products into European markets. • Failure to obtain marketing approval in foreign jurisdictions would prevent our product candidates from being marketed abroad and may limit our ability to generate revenue from product sales. • Our relationships with customers, health care providers, physicians, and third-party payors are subject, directly or indirectly, to federal and state healthcare anti-kickback and fraud and abuse laws, false claims laws, health information privacy and security laws, and other healthcare laws and regulations, which could expose us to criminal sanctions, civil penalties, exclusion from government healthcare programs, contractual damages, reputational harm, and diminished future profits and earnings. If we are unable to comply or have not fully complied with these laws, we could face substantial penalties. • We may face potential liability under applicable privacy laws if we obtain identifiable patient health information from clinical trials sponsored by us. • We are subject to anti-corruption laws, as well as export control, anti-money laundering, customs, sanctions, and other trade laws and regulations governing our operations. Compliance with these legal standards could impair our ability to compete in domestic and international markets. If we fail to comply with these laws, we could be subject to civil or criminal penalties, other remedial measures, and the payment of legal expenses, which could adversely affect our business, results of operations, and financial condition. Confidential 5 5

Risk Factors Risks Related to Intellectual Property • Many aspects of the SynCardia TAH are no longer protected by patents, and we may be unable to protect our products from competition through other means. • The medical device industry is characterized by extensive patent litigation, and we could become subject to litigation that could be costly, result in the diversion of management’s attention, require us to pay significant damages or royalty payments or prevent SynCardia from marketing and selling its existing or future products. • If we fail to comply with our obligations in agreements under which we license rights to technology from third parties, or if the license agreements are terminated for other reasons, we could lose license rights that are important to our business. • We may be subject to claims that we or our employees have inadvertently or intentionally used or disclosed trade secrets or other proprietary information of former employers of our employees. • We may initiate, become a defendant in, or otherwise become party to lawsuits to protect or enforce our intellectual property rights, which could be expensive, time-consuming, and unsuccessful. Risks Related to Altitude and the Business Combination • Altitude and the Company may not be able to obtain the required shareholder approvals to consummate the Business Combination. • The consummation of the Business Combination is subject to risks that regulatory approvals are not obtained, are delayed, or are subject to unanticipated conditions that could adversely affect the combined company or the expected benefits of the Business Combination. • Altitude’s sponsor, officers and directors have potential conflicts of interest in recommending that its stockholders vote in favor of approval of the Business Combination. • Altitude’s sponsor holds approximately 82% of the Company’s outstanding common stock and accordingly will be able to approve the Business Combination even if no other shares are voted in favor of it. Altitude’s sponsor has agreed to vote in favor of the Business Combination, regardless of how public stockholders vote. • Altitude’s sponsor, directors, officers, advisors, and their affiliates may enter into certain transactions, including purchasing shares or warrants from public stockholders, which may influence a vote on the Business Combination and reduce the public “float” of its securities. • Each of Altitude and the Company has incurred and will incur substantial costs in connection with the Business Combination, and related transactions, such as legal, accounting, consulting, and financial advisory fees, which will be paid out of the proceeds of the Business Combination. • The ability of Altitude’s public stockholders to exercise redemption rights with respect to a large number of shares could deplete Altitude’s trust account prior to the Business Combination and thereby diminish the amount of working capital of the combined company. • Subsequent to the consummation of the Business Combination, the combined company may be required to take write-downs or write-offs and restructuring, impairment, or other charges that could have a significant negative effect on its financial condition, results of operations, and share price, which could cause you to lose some or all of your investment. • Uncertainty about the effect of the Business Combination may affect the Company’s ability to retain key employees and integrate management structures and may materially impact the management, strategy, and results of its operation as a combined company. • Altitude is an emerging growth company subject to reduced disclosure requirements, and there is a risk that availing itself of such reduced disclosure requirements will make its common stock less attractive to investors. • The consummation of the Business Combination is subject to a number of conditions, and, if those conditions are not satisfied or waived, the Business Combination agreement may be terminated in accordance with its terms and the Business Combination may not be completed. • Legal proceedings in connection with the Business Combination, the outcomes of which are uncertain, could delay or prevent the completion of the Business Combination. • Changes to the proposed structure of the Business Combination may be required as a result of applicable laws or regulations. • Altitude and the Company will be subject to business uncertainties and contractual restrictions while the Business Combination is pending, and such uncertainty could have a material adverse effect on Altitude’s and the Company’s business, financial condition, and results of operations. • If Altitude is deemed to be an investment company under the Investment Company Act, it may be required to institute burdensome compliance requirements and its activities may be restricted, which may make it difficult to complete the Business Combination. • If Altitude is unable to complete the Business Combination or another initial business combination by December 11, 2023, Altitude will cease all operations except for the purpose of winding up, redeeming 100% of the outstanding public shares, and, subject to the approval of its remaining shareholders and Altitude’s board of directors, dissolving and liquidating. In such event, third parties may bring claims against Altitude and, as a result, the proceeds held in the trust account could be reduced and the per-share liquidation price received by shareholders could be less than $10.00 per share. • The combined company may not be able to realize the anticipated benefits of the Business Combination. Confidential 6 6

Risk Factors Risks Related the Combined Company’s Securities Following Consummation of the Business Combination • The requirements of being a public company may strain our resources, divert management’s attention, and affect our ability to attract and retain executive management and qualified board members. • If, following the Business Combination, securities or industry analysts do not publish or cease publishing research or reports about the combined company, its business, or its market, or if they change their recommendations regarding the combined company’s securities adversely, the price and trading volume of the combined company’s securities could decline. • An active trading market for the combined company’s shares of common stock may not be available on a consistent basis to provide stockholders with adequate liquidity. The stock price may be volatile, and stockholders could lose all or a significant part of their investment. • Following the completion of the Business Combination, SynCardia or its principal stockholders may control a significant percentage of the voting power and will be able to exert significant control over the direction of the business. Such concentration of ownership may affect the market demand for the combined company’s shares. • There can be no assurance that the common stock and warrants issued in connection with the Business Combination will be approved for listing on Nasdaq following the closing, or that the combined company will be able to comply with the continued listing standards of Nasdaq. • Because the Company has no current plans to pay cash dividends for the foreseeable future, you may not receive any return on investment unless you sell your shares for a price greater than that which you paid for them. • Future sales and issuances of the combined company’s common stock or rights to purchase the combined company’s common stock, including pursuant to the combined company’s equity incentive plans, or other equity securities or securities convertible into the combined company’s common stock, including Altitude’s outstanding warrants, could result in additional dilution of the percentage ownership of the combined company’s stockholders and could cause the stock price of the combined company’s common stock to decline even if its business is doing well. • Warrants will become exercisable for the combined company’s common stock beginning 30 days after the closing of the Business Combination, which would increase the number of shares eligible for future resale in the public market and result in dilution to the combined company’s stockholders and could also cause the market price of our common stock to drop significantly, even if our business is doing well. • Stockholders will experience immediate dilution as a consequence of the issuance of common stock as consideration in the Business Combination. Having a minority share position may reduce the influence that stockholders have on the management of the Company. • If we fail to establish and maintain effective internal controls, our ability to produce accurate and timely financial statements could be impaired, which could harm our operating results, investors’ views of us, and, as a result, the value of our common stock. • Our internal controls and procedures may not prevent or detect all errors or acts of fraud. • Changes to, or application of different, financial accounting standards (including PCAOB standards) may result in changes to our results of operations, which changes could be material. • Following the Business Combination, anti-takeover provisions contained in the combined company’s certificate of incorporation and bylaws, as well as provisions of Delaware law, could delay or prevent a change in control, which could reduce the market price the combined company’s common stock and frustrate attempts by our stockholders to make changes in management. • Following the Business Combination, the combined company’s certificate of incorporation and bylaws will provide for an exclusive forum in the Court of Chancery of the State of Delaware for certain disputes between the combined company and its stockholders, and that the federal district courts of the United States will be the exclusive forum for the resolution of any complaint asserting a cause of action under the Securities Act of 1933, as amended, which could discourage claims or limit stockholders’ ability to make a claim against the combined company, its directors, officers, other employees, or stockholders. • The combined company will incur significant expenses as a result of being a public company, which could materially adversely affect the combined company’s business, results of operations, and financial condition. • Our quarterly operating results may fluctuate significantly or may fall below the expectations of investors or securities analysts, each of which may cause our stock price to fluctuate or decline. • After the completion of the Business Combination, we may be at an increased risk of securities class action litigation. Confidential 7 7

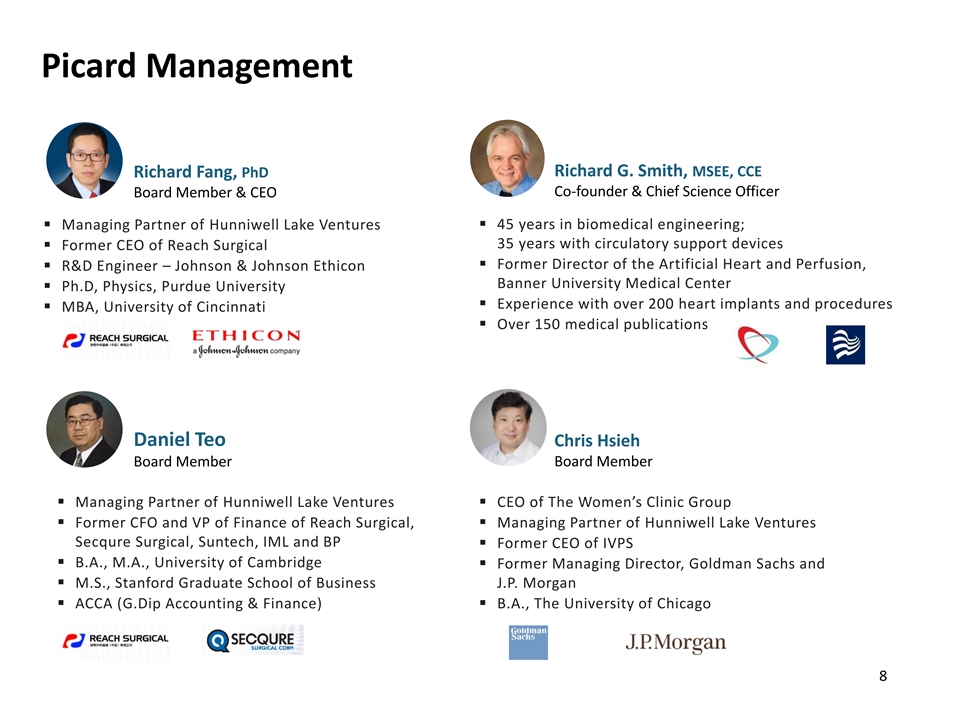

Picard Management Richard G. Smith, MSEE, CCE Richard Fang, PhD Co-founder & Chief Science Officer Board Member & CEO ▪ Managing Partner of Hunniwell Lake Ventures▪ 45 years in biomedical engineering; 35 years with circulatory support devices ▪ Former CEO of Reach Surgical ▪ Former Director of the Artificial Heart and Perfusion, ▪ R&D Engineer – Johnson & Johnson Ethicon Banner University Medical Center ▪ Ph.D, Physics, Purdue University ▪ Experience with over 200 heart implants and procedures ▪ MBA, University of Cincinnati ▪ Over 150 medical publications Daniel Teo Chris Hsieh Board Member Board Member ▪ Managing Partner of Hunniwell Lake Ventures▪ CEO of The Women’s Clinic Group ▪ Former CFO and VP of Finance of Reach Surgical, ▪ Managing Partner of Hunniwell Lake Ventures Secqure Surgical, Suntech, IML and BP ▪ Former CEO of IVPS ▪ B.A., M.A., University of Cambridge ▪ Former Managing Director, Goldman Sachs and ▪ M.S., Stanford Graduate School of Business J.P. Morgan ▪ ACCA (G.Dip Accounting & Finance) ▪ B.A., The University of Chicago Confidential 8 8

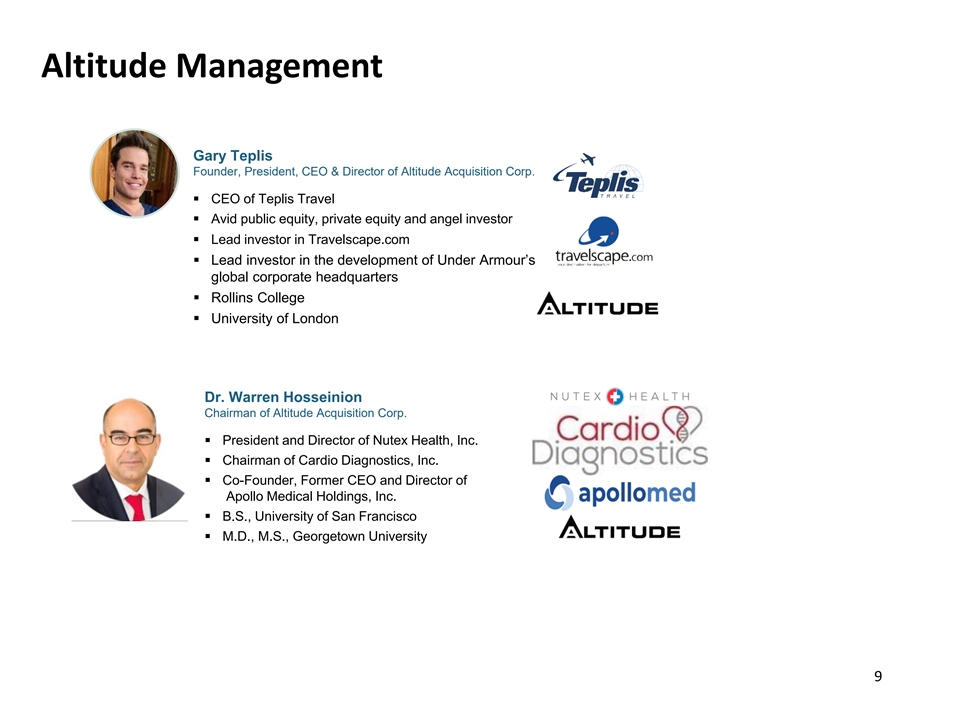

Altitude Management Gary Teplis Founder, President, CEO & Director of Altitude Acquisition Corp. ▪ CEO of Teplis Travel ▪ Avid public equity, private equity and angel investor ▪ Lead investor in Travelscape.com ▪ Lead investor in the development of Under Armour’s global corporate headquarters ▪ Rollins College ▪ University of London Dr. Warren Hosseinion Chairman of Altitude Acquisition Corp. ▪ President and Director of Nutex Health, Inc. ▪ Chairman of Cardio Diagnostics, Inc. ▪ Co-Founder, Former CEO and Director of Apollo Medical Holdings, Inc. ▪ B.S., University of San Francisco ▪ M.D., M.S., Georgetown University Confidential 9 1

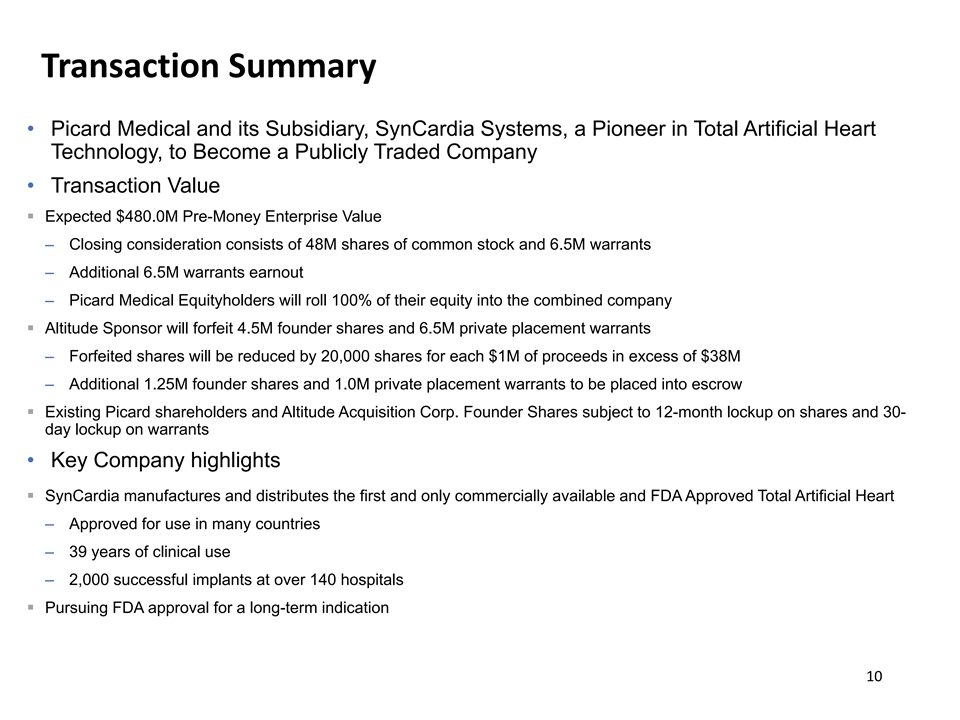

Transaction Summary • Picard Medical and its Subsidiary, SynCardia Systems, a Pioneer in Total Artificial Heart Technology, to Become a Publicly Traded Company • Transaction Value ▪ Expected $480.0M Pre-Money Enterprise Value – Closing consideration consists of 48M shares of common stock and 6.5M warrants – Additional 6.5M warrants earnout – Picard Medical Equityholders will roll 100% of their equity into the combined company ▪ Altitude Sponsor will forfeit 4.5M founder shares and 6.5M private placement warrants – Forfeited shares will be reduced by 20,000 shares for each $1M of proceeds in excess of $38M – Additional 1.25M founder shares and 1.0M private placement warrants to be placed into escrow ▪ Existing Picard shareholders and Altitude Acquisition Corp. Founder Shares subject to 12-month lockup on shares and 30- day lockup on warrants • Key Company highlights ▪ SynCardia manufactures and distributes the first and only commercially available and FDA Approved Total Artificial Heart – Approved for use in many countries – 39 years of clinical use – 2,000 successful implants at over 140 hospitals ▪ Pursuing FDA approval for a long-term indication Confidential 10 10

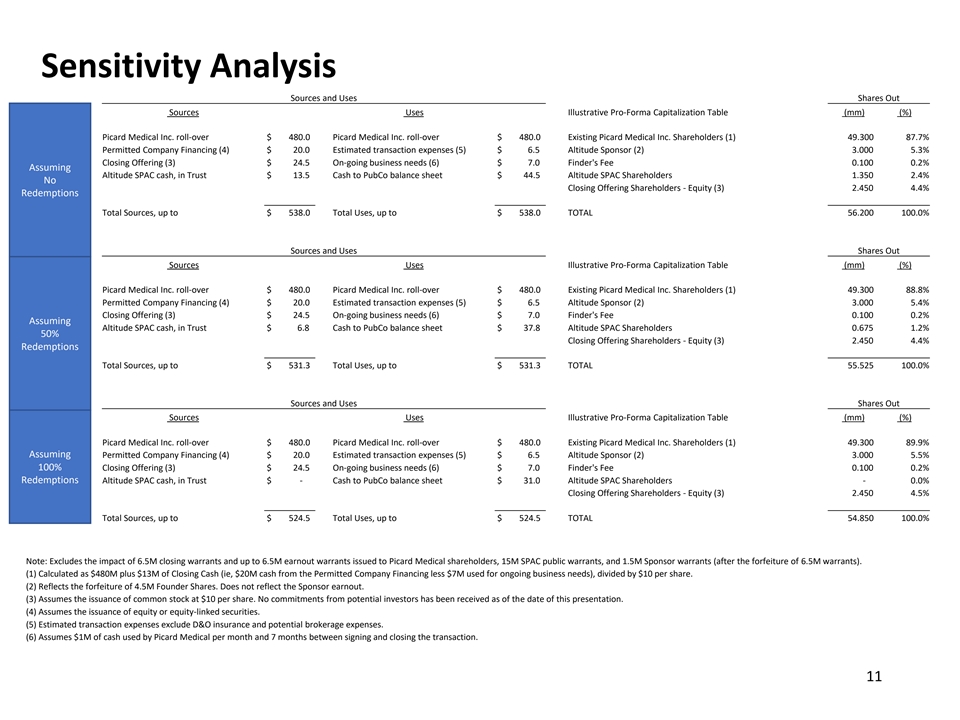

Sensitivity Analysis Sources and Uses Shares Out Sources Uses Illustrative Pro-Forma Capitalization Table (mm) (%) Picard Medical Inc. roll-over $ 480.0 Picard Medical Inc. roll-over $ 480.0 Existing Picard Medical Inc. Shareholders (1) 49.300 87.7% Permitted Company Financing (4) $ 20.0 Estimated transaction expenses (5) $ 6.5 Altitude Sponsor (2) 3.000 5.3% Closing Offering (3) $ 24.5 On-going business needs (6) $ 7.0 Finder's Fee 0.100 0.2% Assuming Altitude SPAC cash, in Trust $ 13.5 Cash to PubCo balance sheet $ 44.5 Altitude SPAC Shareholders 1.350 2.4% No Closing Offering Shareholders - Equity (3) 2.450 4.4% Redemptions Total Sources, up to $ 538.0 Total Uses, up to $ 538.0 TOTAL 56.200 100.0% Sources and Uses Shares Out Sources Uses Illustrative Pro-Forma Capitalization Table (mm) (%) Picard Medical Inc. roll-over $ 480.0 Picard Medical Inc. roll-over $ 480.0 Existing Picard Medical Inc. Shareholders (1) 49.300 88.8% Permitted Company Financing (4) $ 20.0 Estimated transaction expenses (5) $ 6.5 Altitude Sponsor (2) 3.000 5.4% Closing Offering (3) $ 24.5 On-going business needs (6) $ 7.0 Finder's Fee 0.100 0.2% Assuming Altitude SPAC cash, in Trust $ 6.8 Cash to PubCo balance sheet $ 37.8 Altitude SPAC Shareholders 0.675 1.2% 50% Closing Offering Shareholders - Equity (3) 2.450 4.4% Redemptions Total Sources, up to $ 531.3 Total Uses, up to $ 531.3 TOTAL 55.525 100.0% Sources and Uses Shares Out Sources Uses Illustrative Pro-Forma Capitalization Table (mm) (%) Picard Medical Inc. roll-over $ 480.0 Picard Medical Inc. roll-over $ 480.0 Existing Picard Medical Inc. Shareholders (1) 49.300 89.9% Assuming Permitted Company Financing (4) $ 20.0 Estimated transaction expenses (5) $ 6.5 Altitude Sponsor (2) 3.000 5.5% 100% Closing Offering (3) $ 24.5 On-going business needs (6) $ 7.0 Finder's Fee 0.100 0.2% Redemptions Altitude SPAC cash, in Trust $ - Cash to PubCo balance sheet $ 31.0 Altitude SPAC Shareholders - 0.0% Closing Offering Shareholders - Equity (3) 2.450 4.5% Total Sources, up to $ 524.5 Total Uses, up to $ 524.5 TOTAL 54.850 100.0% Note: Excludes the impact of 6.5M closing warrants and up to 6.5M earnout warrants issued to Picard Medical shareholders, 15M SPAC public warrants, and 1.5M Sponsor warrants (after the forfeiture of 6.5M warrants). (1) Calculated as $480M plus $13M of Closing Cash (ie, $20M cash from the Permitted Company Financing less $7M used for ongoing business needs), divided by $10 per share. (2) Reflects the forfeiture of 4.5M Founder Shares. Does not reflect the Sponsor earnout. (3) Assumes the issuance of common stock at $10 per share. No commitments from potential investors has been received as of the date of this presentation. (4) Assumes the issuance of equity or equity-linked securities. (5) Estimated transaction expenses exclude D&O insurance and potential brokerage expenses. (6) Assumes $1M of cash used by Picard Medical per month and 7 months between signing and closing the transaction. Confidential 11 11

SynCardia at-a-Glance ▪ SynCardia’s Total Artificial Heart (TAH) replaces full functions of a failing or failed human heart ▪ Designed to address unmet and growing needs in multibillion-dollar markets in the U.S. and globally ▪ Approved for use in over 30 countries, including the U.S., Canada, UK, and all major EU countries ▪ Commercially-available with over 2,000 implants completed in over 20 countries ▪ Strong clinical data expected to support and expand U.S. FDA Indications from bridge-to-transplant (BTT) to long-term or destination therapies ▪ Major product upgrades expected in near future and more new products driving further demand ▪ Growing international recognition and expansion into China, Middle East, India and other Asian countries Confident12 ial 12

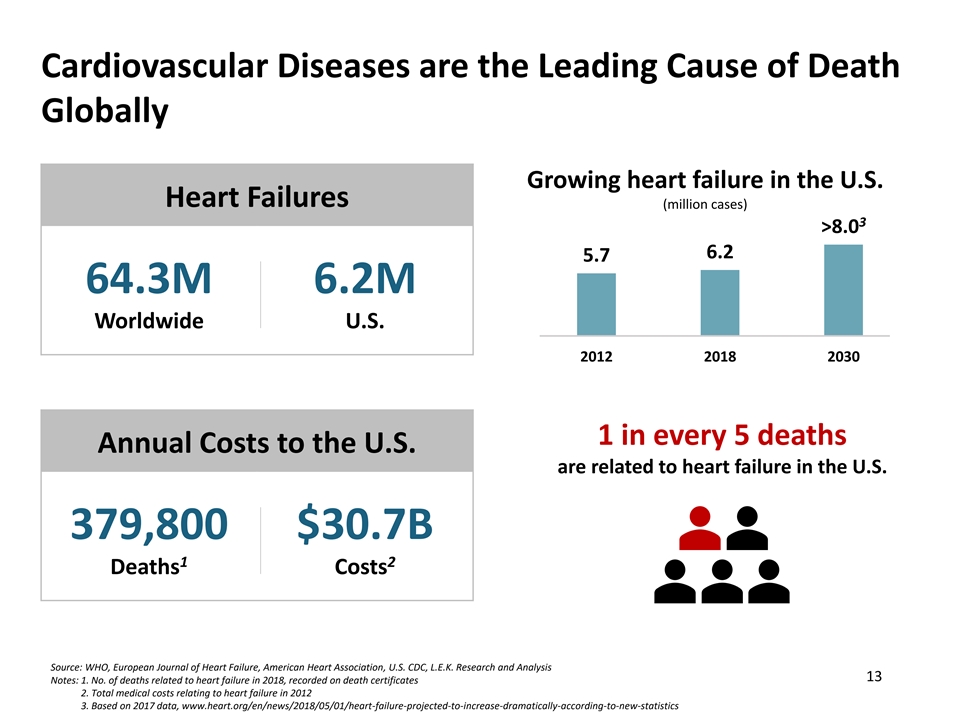

Cardiovascular Diseases are the Leading Cause of Death Globally Growing heart failure in the U.S. Heart Failures (million cases) 3 >8.0 6.2 5.7 64.3M 6.2M Worldwide U.S. 2012 2018 2030 1 in every 5 deaths Annual Costs to the U.S. are related to heart failure in the U.S. 379,800 $30.7B 1 2 Deaths Costs Source: WHO, European Journal of Heart Failure, American Heart Association, U.S. CDC, L.E.K. Research and Analysis Confidential 13 Notes: 1. No. of deaths related to heart failure in 2018, recorded on death certificates 13 2. Total medical costs relating to heart failure in 2012 3. Based on 2017 data, www.heart.org/en/news/2018/05/01/heart-failure-projected-to-increase-dramatically-according-to-new-statistics

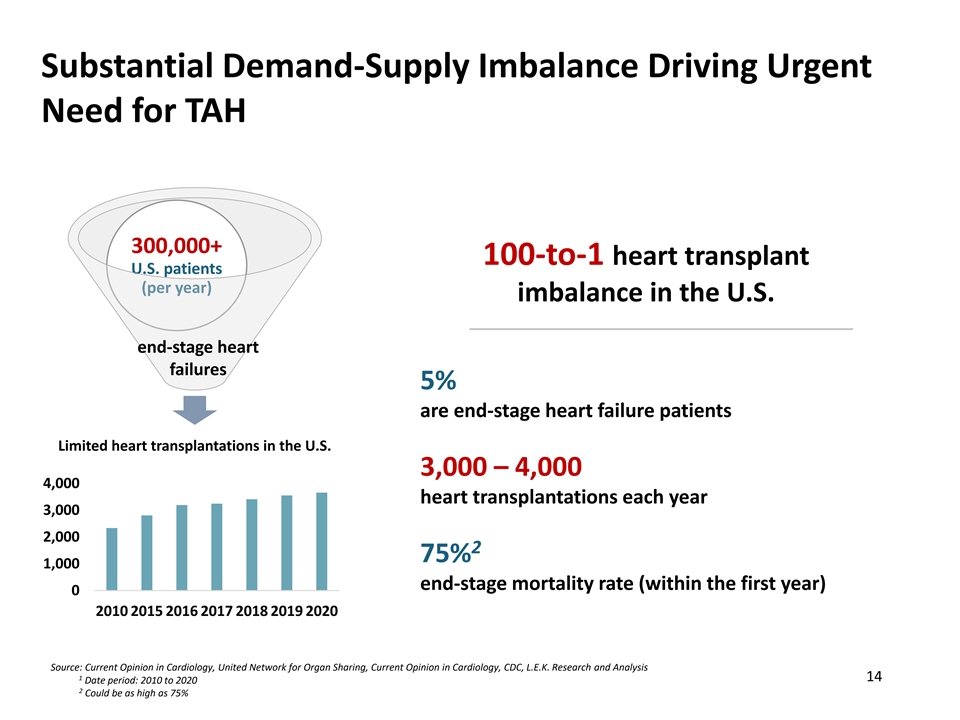

Substantial Demand-Supply Imbalance Driving Urgent Need for TAH 300,000+ 100-to-1 heart transplant U.S. patients (per year) imbalance in the U.S. end-stage heart failures 5% are end-stage heart failure patients Limited heart transplantations in the U.S. 3,000 – 4,000 4,000 heart transplantations each year 3,000 2,000 2 75% 1,000 end-stage mortality rate (within the first year) 0 2010 2015 2016 2017 2018 2019 2020 Source: Current Opinion in Cardiology, United Network for Organ Sharing, Current Opinion in Cardiology, CDC, L.E.K. Research and Analysis Confidential 1 14 Date period: 2010 to 2020 14 2 Could be as high as 75%

1 Our Solution: The First and Only Commercially-Available Total Artificial Heart (TAH) in the U.S. Replacement to full functions of a human heart for end-stage, biventricular heart failure Obtained approvals from: U.S. Canada Source: SynCardia Confidential 1 15 Note: Based on company’s review of publicly available information 15

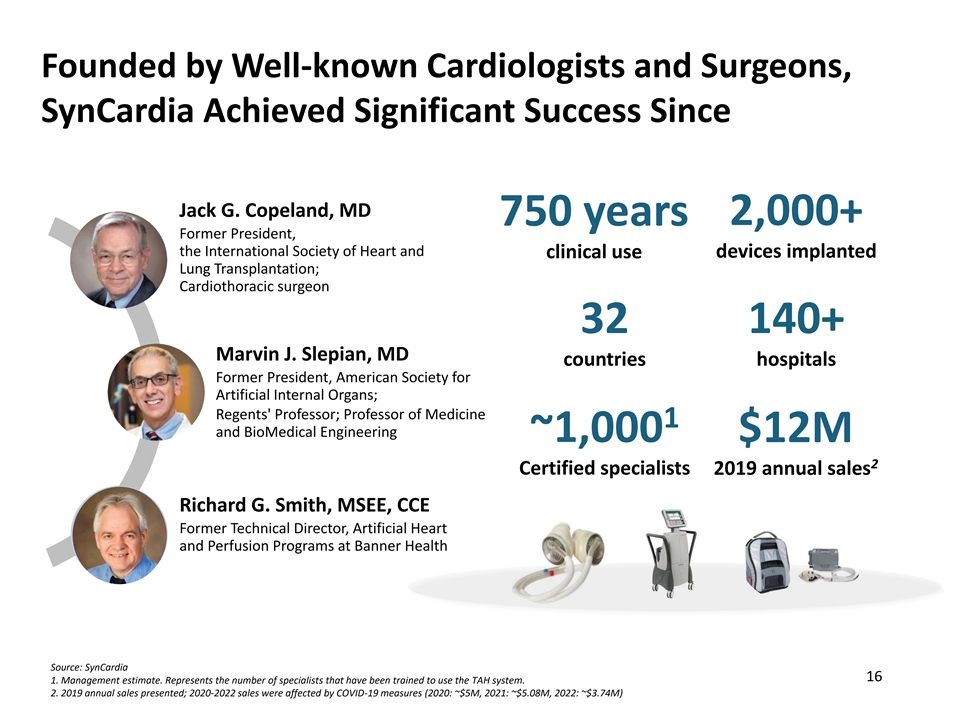

Founded by Well-known Cardiologists and Surgeons, SynCardia Achieved Significant Success Since Jack G. Copeland, MD 750 years 2,000+ Former President, the International Society of Heart and devices implanted clinical use Lung Transplantation; Cardiothoracic surgeon 32 140+ Marvin J. Slepian, MD countries hospitals Former President, American Society for Artificial Internal Organs; Regents' Professor; Professor of Medicine 1 and BioMedical Engineering ~1,000 $12M 2 Certified specialists 2019 annual sales Richard G. Smith, MSEE, CCE Former Technical Director, Artificial Heart and Perfusion Programs at Banner Health Source: SynCardia Confidential 16 1. Management estimate. Represents the number of specialists that have been trained to use the TAH system. 16 2. 2019 annual sales presented; 2020-2022 sales were affected by COVID-19 measures (2020: ~$5M, 2021: ~$5.08M, 2022: ~$3.74M)

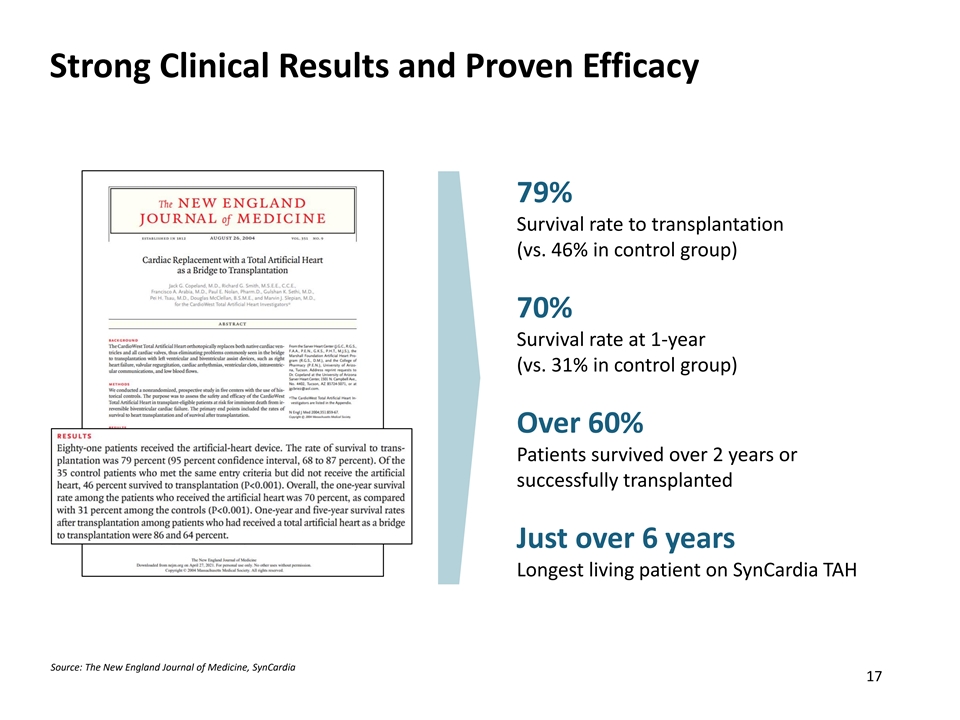

Strong Clinical Results and Proven Efficacy 79% Survival rate to transplantation (vs. 46% in control group) 70% Survival rate at 1-year (vs. 31% in control group) Over 60% Patients survived over 2 years or successfully transplanted Just over 6 years Longest living patient on SynCardia TAH Source: The New England Journal of Medicine, SynCardia Confidential 17 17

Prolonging and Enabling High-Quality Lives Jahiem, 11, supported by Stan, 23, played basketball wearing SynCardia TAH for 280 days Freedom® Portable Driver in the backpack Mohamad, 27, the first TAH transplant in Lebanon Randy, 39, completed the 4.2-mile Pat’s Run event Bob, 55, went on hunting trips using the SynCardia TAH Chris, 51, hiked a total of 607 miles after TAH transplantation Andrei, 12, one of the youngest Nurullah, 61, supported by patients from Italy SynCardia TAH for over 1,700 days Source: SynCardia Confidential 18 18

Capturing the Growing Opportunity Confidential 19 19

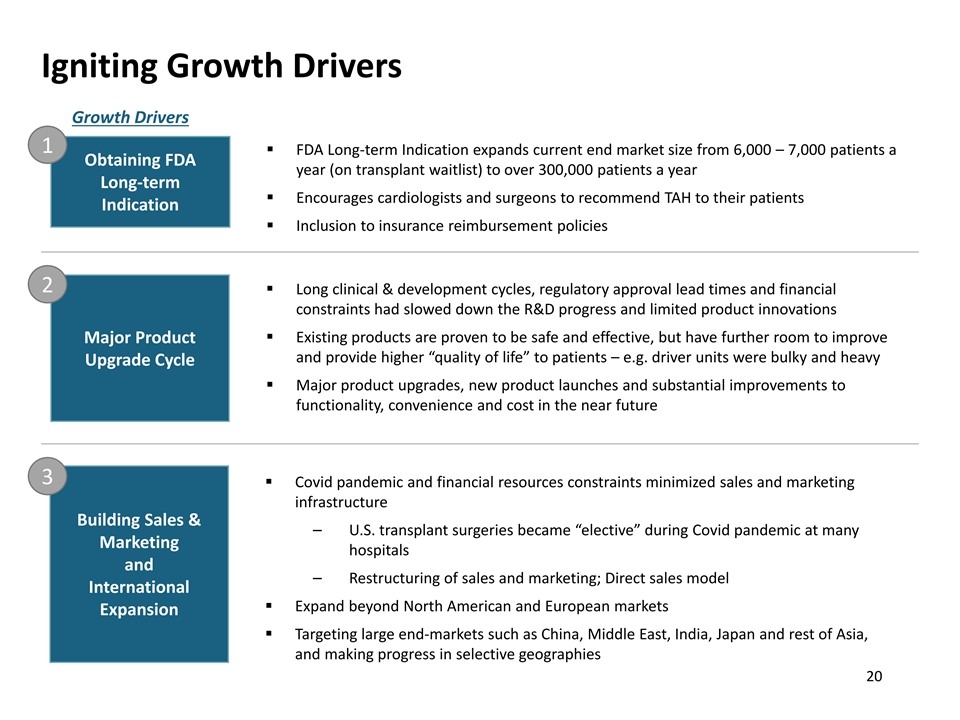

Igniting Growth Drivers Growth Drivers 1 ▪ FDA Long-term Indication expands current end market size from 6,000 – 7,000 patients a Obtaining FDA year (on transplant waitlist) to over 300,000 patients a year Long-term ▪ Encourages cardiologists and surgeons to recommend TAH to their patients Indication ▪ Inclusion to insurance reimbursement policies 2 ▪ Long clinical & development cycles, regulatory approval lead times and financial constraints had slowed down the R&D progress and limited product innovations ▪ Existing products are proven to be safe and effective, but have further room to improve Major Product and provide higher “quality of life” to patients – e.g. driver units were bulky and heavy Upgrade Cycle ▪ Major product upgrades, new product launches and substantial improvements to functionality, convenience and cost in the near future 3 ▪ Covid pandemic and financial resources constraints minimized sales and marketing infrastructure Building Sales & ⎯ U.S. transplant surgeries became “elective” during Covid pandemic at many Marketing hospitals and ⎯ Restructuring of sales and marketing; Direct sales model International ▪ Expand beyond North American and European markets Expansion ▪ Targeting large end-markets such as China, Middle East, India, Japan and rest of Asia, and making progress in selective geographies Confidential 20 20

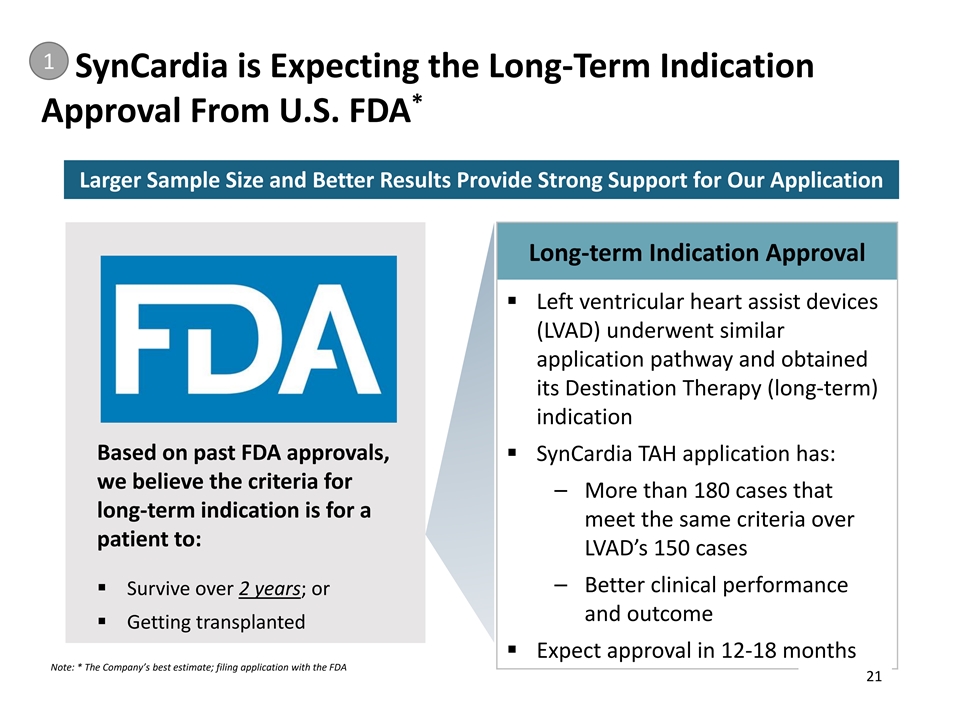

1 SynCardia is Expecting the Long-Term Indication * Approval From U.S. FDA Larger Sample Size and Better Results Provide Strong Support for Our Application Long-term Indication Approval ▪ Left ventricular heart assist devices (LVAD) underwent similar application pathway and obtained its Destination Therapy (long-term) indication Based on past FDA approvals, ▪ SynCardia TAH application has: we believe the criteria for ⎯ More than 180 cases that long-term indication is for a meet the same criteria over patient to: LVAD’s 150 cases ⎯ Better clinical performance ▪ Survive over 2 years; or and outcome ▪ Getting transplanted ▪ Expect approval in 12-18 months Note: * The Company’s best estimate; filing application with the FDA Confidential 21 21

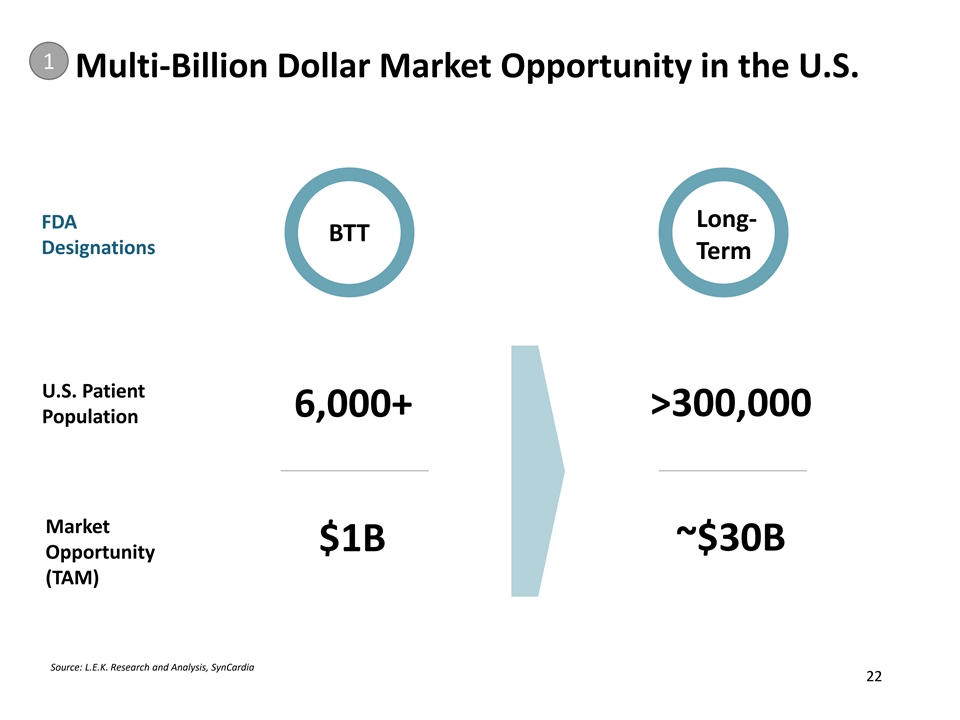

1 Multi-Billion Dollar Market Opportunity in the U.S. Long- FDA B BT TT T Designations Term U.S. Patient >300,000 6,000+ Population Market ~$30B $1B Opportunity (TAM) Source: L.E.K. Research and Analysis, SynCardia Confidential 22 22

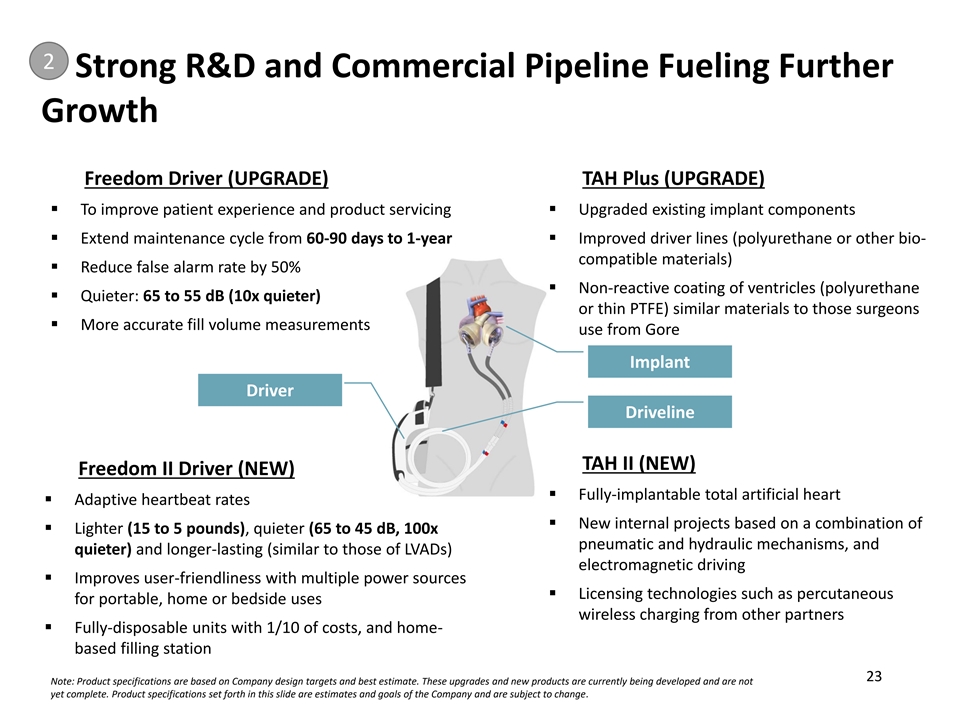

2 Strong R&D and Commercial Pipeline Fueling Further Growth Freedom Driver (UPGRADE) TAH Plus (UPGRADE) ▪ To improve patient experience and product servicing▪ Upgraded existing implant components ▪ Extend maintenance cycle from 60-90 days to 1-year▪ Improved driver lines (polyurethane or other bio- compatible materials) ▪ Reduce false alarm rate by 50% ▪ Non-reactive coating of ventricles (polyurethane ▪ Quieter: 65 to 55 dB (10x quieter) or thin PTFE) similar materials to those surgeons ▪ More accurate fill volume measurements use from Gore Implant Driver Driveline TAH II (NEW) Freedom II Driver (NEW) ▪ Fully-implantable total artificial heart ▪ Adaptive heartbeat rates ▪ New internal projects based on a combination of ▪ Lighter (15 to 5 pounds), quieter (65 to 45 dB, 100x pneumatic and hydraulic mechanisms, and quieter) and longer-lasting (similar to those of LVADs) electromagnetic driving ▪ Improves user-friendliness with multiple power sources ▪ Licensing technologies such as percutaneous for portable, home or bedside uses wireless charging from other partners ▪ Fully-disposable units with 1/10 of costs, and home- based filling station Confidential 23 Note: Product specifications are based on Company design targets and best estimate. These upgrades and new products are currently being developed and are not 23 yet complete. Product specifications set forth in this slide are estimates and goals of the Company and are subject to change.

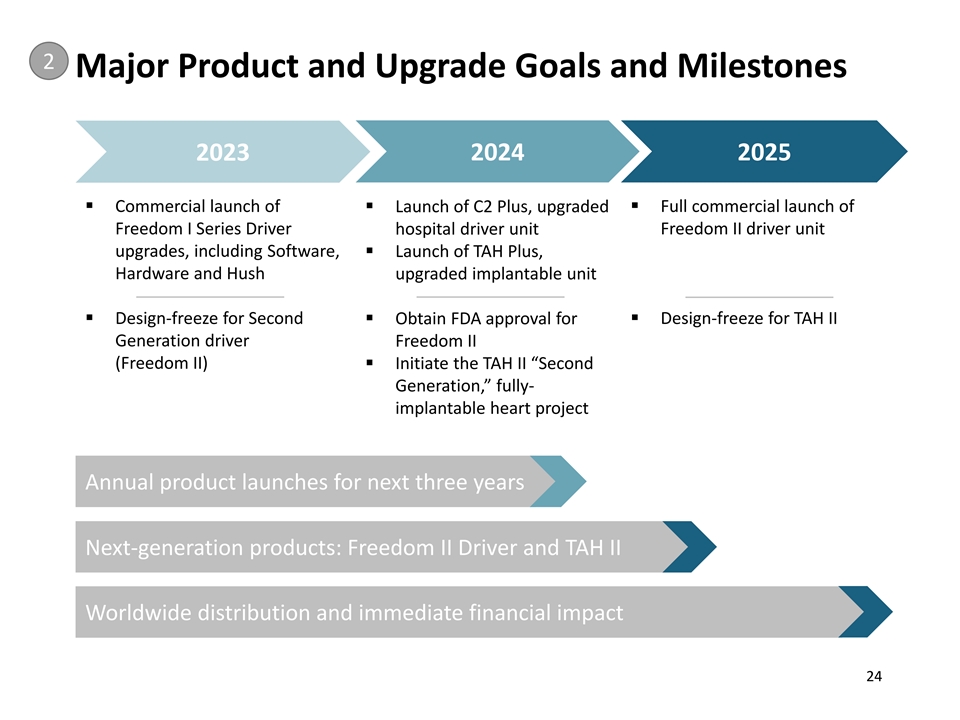

2 Major Product and Upgrade Goals and Milestones 2023 2024 2025 ▪ Commercial launch of ▪ Launch of C2 Plus, upgraded ▪ Full commercial launch of Freedom I Series Driver hospital driver unit Freedom II driver unit upgrades, including Software, ▪ Launch of TAH Plus, Hardware and Hush upgraded implantable unit ▪ Design-freeze for Second ▪ Obtain FDA approval for ▪ Design-freeze for TAH II Generation driver Freedom II (Freedom II)▪ Initiate the TAH II “Second Generation,” fully- implantable heart project Annual product launches for next three years Next-generation products: Freedom II Driver and TAH II Worldwide distribution and immediate financial impact Confidential 24 24

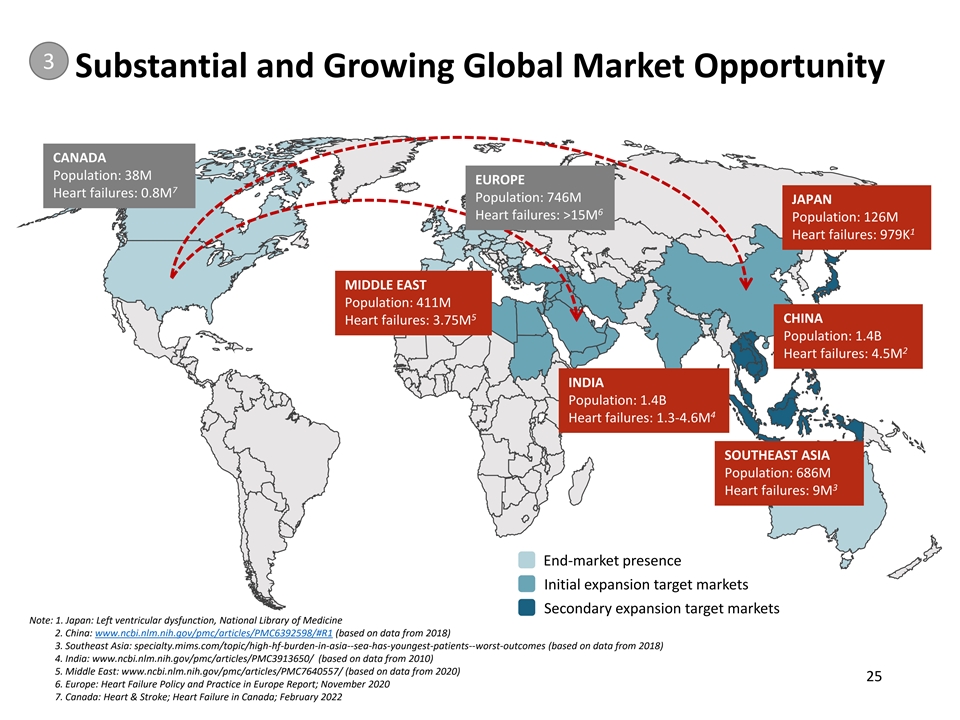

3 Substantial and Growing Global Market Opportunity CANADA Population: 38M EUROPE 7 Heart failures: 0.8M Population: 746M JAPAN 6 Heart failures: >15M Population: 126M 1 Heart failures: 979K MIDDLE EAST Population: 411M 5 CHINA Heart failures: 3.75M Population: 1.4B 2 Heart failures: 4.5M INDIA Population: 1.4B 4 Heart failures: 1.3-4.6M SOUTHEAST ASIA Population: 686M 3 Heart failures: 9M End-market presence Initial expansion target markets Secondary expansion target markets Note: 1. Japan: Left ventricular dysfunction, National Library of Medicine 2. China: www.ncbi.nlm.nih.gov/pmc/articles/PMC6392598/#R1 (based on data from 2018) 3. Southeast Asia: specialty.mims.com/topic/high-hf-burden-in-asia--sea-has-youngest-patients--worst-outcomes (based on data from 2018) 4. India: www.ncbi.nlm.nih.gov/pmc/articles/PMC3913650/ (based on data from 2010) Confidential 5. Middle East: www.ncbi.nlm.nih.gov/pmc/articles/PMC7640557/ (based on data from 2020) 25 6. Europe: Heart Failure Policy and Practice in Europe Report; November 2020 25 7. Canada: Heart & Stroke; Heart Failure in Canada; February 2022

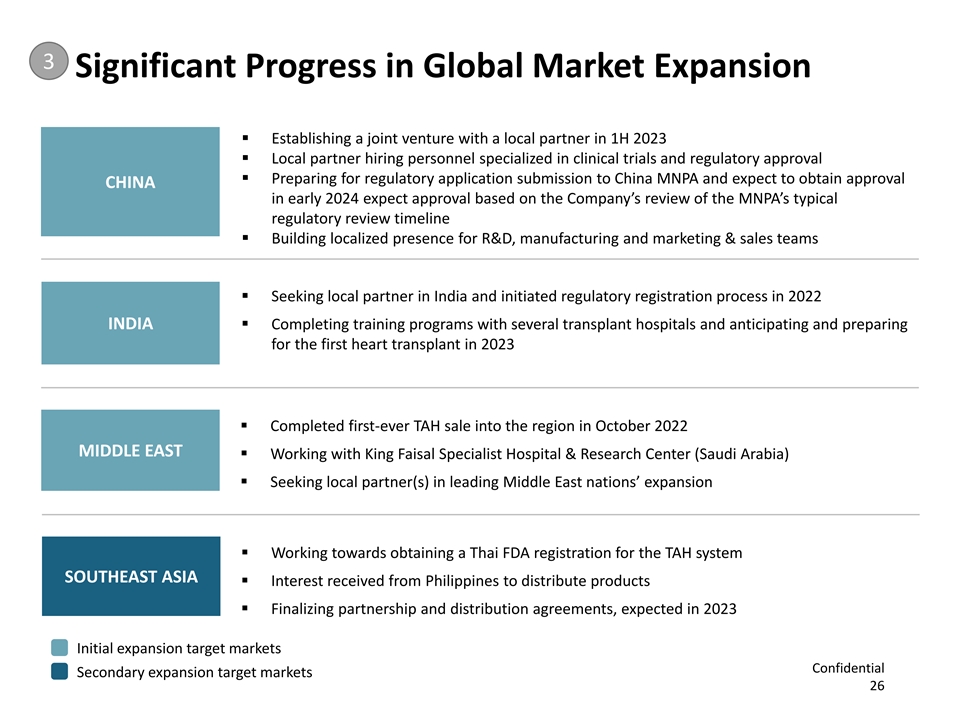

3 Significant Progress in Global Market Expansion ▪ Establishing a joint venture with a local partner in 1H 2023 ▪ Local partner hiring personnel specialized in clinical trials and regulatory approval ▪ Preparing for regulatory application submission to China MNPA and expect to obtain approval CHINA in early 2024 expect approval based on the Company’s review of the MNPA’s typical regulatory review timeline ▪ Building localized presence for R&D, manufacturing and marketing & sales teams ▪ Seeking local partner in India and initiated regulatory registration process in 2022 INDIA▪ Completing training programs with several transplant hospitals and anticipating and preparing for the first heart transplant in 2023 ▪ Completed first-ever TAH sale into the region in October 2022 MIDDLE EAST ▪ Working with King Faisal Specialist Hospital & Research Center (Saudi Arabia) ▪ Seeking local partner(s) in leading Middle East nations’ expansion ▪ Working towards obtaining a Thai FDA registration for the TAH system SOUTHEAST ASIA ▪ Interest received from Philippines to distribute products ▪ Finalizing partnership and distribution agreements, expected in 2023 Initial expansion target markets Confidential Secondary expansion target markets 26

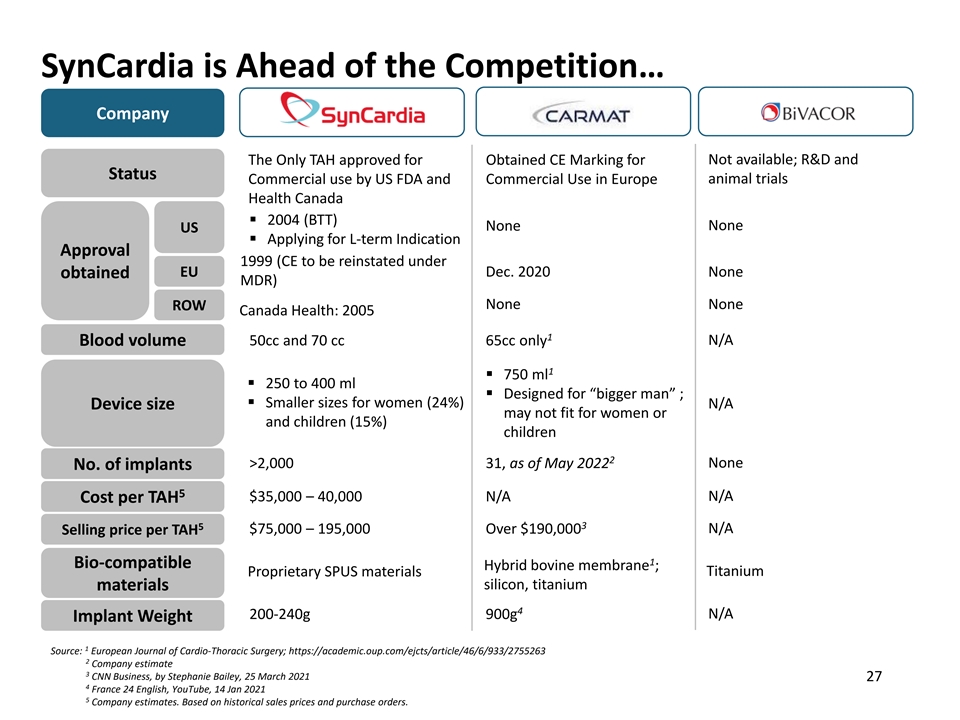

SynCardia is Ahead of the Competition… Company Not available; R&D and The Only TAH approved for Obtained CE Marking for Status Commercial use by US FDA and Commercial Use in Europe animal trials Health Canada ▪ 2004 (BTT) None None US ▪ Applying for L-term Indication Approval 1999 (CE to be reinstated under EU Dec. 2020 None obtained MDR) None None ROW Canada Health: 2005 1 50cc and 70 cc 65cc only N/A Blood volume 1 ▪ 750 ml ▪ 250 to 400 ml ▪ Designed for “bigger man” ; ▪ Smaller sizes for women (24%) Device size N/A may not fit for women or and children (15%) children 2 >2,000 31, as of May 2022 None No. of implants 5 $35,000 – 40,000 N/A N/A Cost per TAH 3 5 $75,000 – 195,000 Over $190,000 N/A Selling price per TAH 1 Bio-compatible Hybrid bovine membrane ; Titanium Proprietary SPUS materials silicon, titanium materials 4 200-240g 900g N/A Implant Weight 1 Source: European Journal of Cardio-Thoracic Surgery; https://academic.oup.com/ejcts/article/46/6/933/2755263 2 Company estimate Confidential 3 CNN Business, by Stephanie Bailey, 25 March 2021 27 4 27 France 24 English, YouTube, 14 Jan 2021 5 Company estimates. Based on historical sales prices and purchase orders.

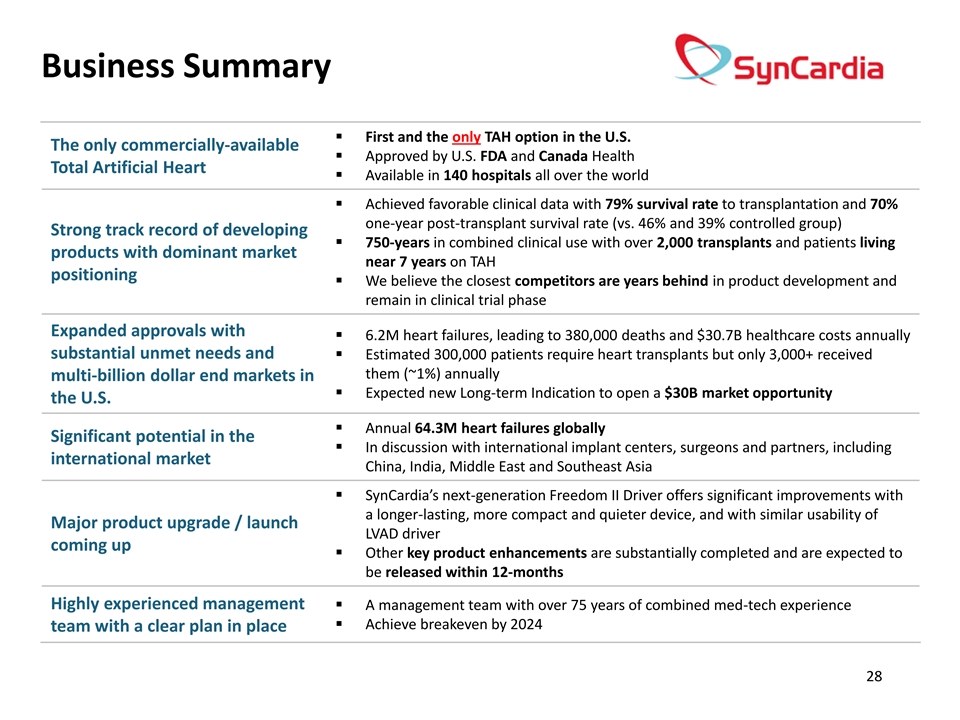

Business Summary ▪ First and the only TAH option in the U.S. The only commercially-available ▪ Approved by U.S. FDA and Canada Health Total Artificial Heart ▪ Available in 140 hospitals all over the world ▪ Achieved favorable clinical data with 79% survival rate to transplantation and 70% one-year post-transplant survival rate (vs. 46% and 39% controlled group) Strong track record of developing ▪ 750-years in combined clinical use with over 2,000 transplants and patients living products with dominant market near 7 years on TAH positioning ▪ We believe the closest competitors are years behind in product development and remain in clinical trial phase Expanded approvals with ▪ 6.2M heart failures, leading to 380,000 deaths and $30.7B healthcare costs annually substantial unmet needs and ▪ Estimated 300,000 patients require heart transplants but only 3,000+ received them (~1%) annually multi-billion dollar end markets in ▪ Expected new Long-term Indication to open a $30B market opportunity the U.S. ▪ Annual 64.3M heart failures globally Significant potential in the ▪ In discussion with international implant centers, surgeons and partners, including international market China, India, Middle East and Southeast Asia ▪ SynCardia’s next-generation Freedom II Driver offers significant improvements with a longer-lasting, more compact and quieter device, and with similar usability of Major product upgrade / launch LVAD driver coming up ▪ Other key product enhancements are substantially completed and are expected to be released within 12-months Highly experienced management ▪ A management team with over 75 years of combined med-tech experience ▪ Achieve breakeven by 2024 team with a clear plan in place Confidential 28 28

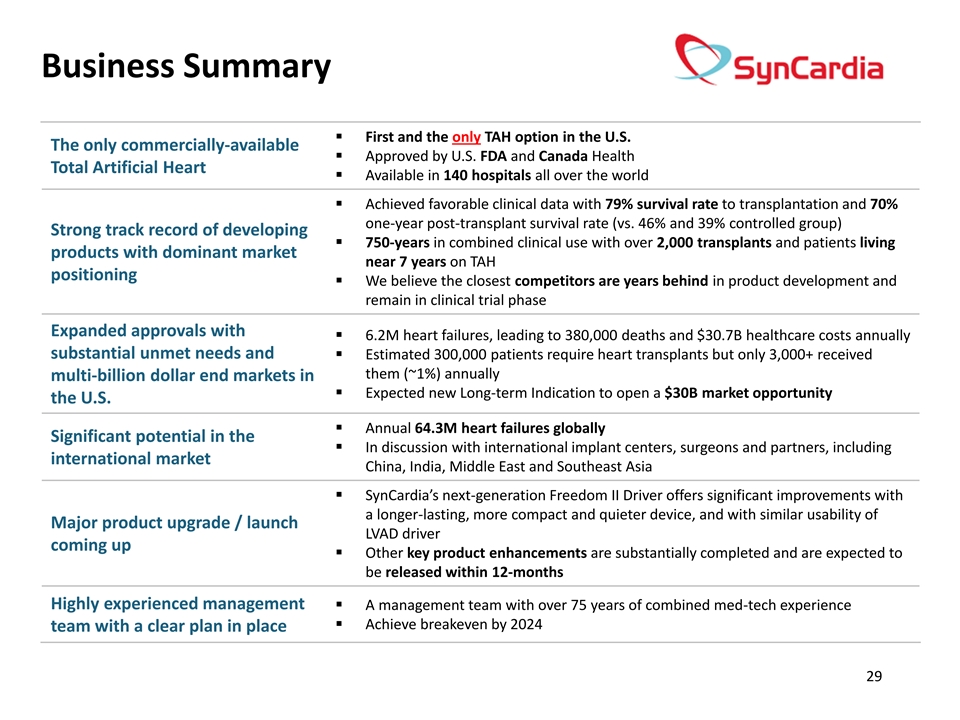

Business Summary ▪ First and the only TAH option in the U.S. The only commercially-available ▪ Approved by U.S. FDA and Canada Health Total Artificial Heart ▪ Available in 140 hospitals all over the world ▪ Achieved favorable clinical data with 79% survival rate to transplantation and 70% one-year post-transplant survival rate (vs. 46% and 39% controlled group) Strong track record of developing ▪ 750-years in combined clinical use with over 2,000 transplants and patients living products with dominant market near 7 years on TAH positioning ▪ We believe the closest competitors are years behind in product development and remain in clinical trial phase Expanded approvals with ▪ 6.2M heart failures, leading to 380,000 deaths and $30.7B healthcare costs annually substantial unmet needs and ▪ Estimated 300,000 patients require heart transplants but only 3,000+ received them (~1%) annually multi-billion dollar end markets in ▪ Expected new Long-term Indication to open a $30B market opportunity the U.S. ▪ Annual 64.3M heart failures globally Significant potential in the ▪ In discussion with international implant centers, surgeons and partners, including international market China, India, Middle East and Southeast Asia ▪ SynCardia’s next-generation Freedom II Driver offers significant improvements with a longer-lasting, more compact and quieter device, and with similar usability of Major product upgrade / launch LVAD driver coming up ▪ Other key product enhancements are substantially completed and are expected to be released within 12-months Highly experienced management ▪ A management team with over 75 years of combined med-tech experience ▪ Achieve breakeven by 2024 team with a clear plan in place Confidential 29 29